I can not ascertain as to the reasons banking companies do earnestly strive for their customers so you’re able to re-finance its mortgage from the a lowered interest. And to be certainly clear, I am talking about a bank refinancing a loan at the its very own lender (Wells Fargo refinancing financing out of Wells Fargo). Preciselywhat are its incentives?

- They generate some funds throughout the settlement costs

- They resets the fresh amortization agenda and that means you is actually investing a higher percentage of your percentage while the attract

Although differences is not much after you possess simply had the previous financing for most decades. And you will what is very confusing is that financial institutions in the usa correct now are offering refinancing and no settlement costs.

I would personally want to take advantage of one among them zero-costs closing refinances but I am afraid that we have to be missing one thing huge in case the banking institutions are making an effort to save yourself myself money. New crazy procedure is the fact I can refinance my 30 seasons (at which I have twenty seven ages commit) towards the an effective 20 season in the a lowered interest and you can spend nearly a comparable matter four weeks. What are We lost?

What’s the incentive for a bank so you can re-finance a mortgage on a diminished rate?

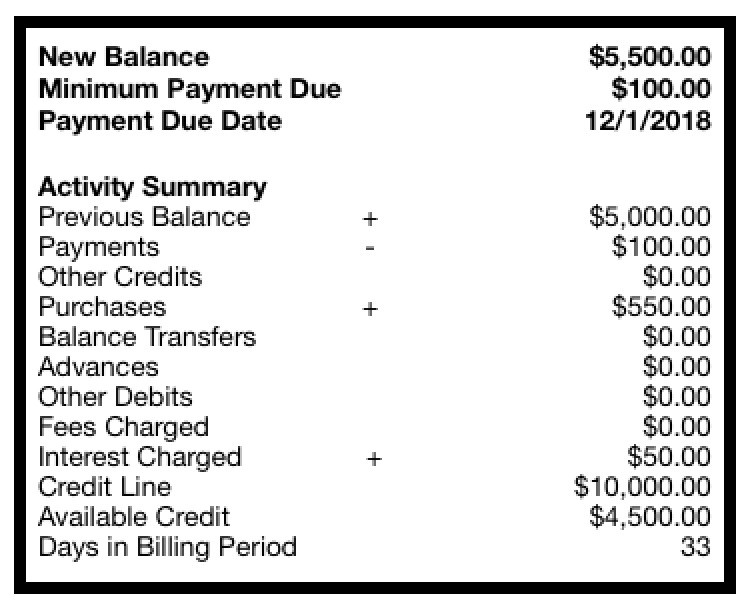

This can be a thirty seasons $402k fixed at cuatro.875% having 27 ages kept refinanced to help you 20 season fixed on cuatro.125%. Monthly payment goes away from $dos, to $dos,. How is it a tremendous amount to own Wells Fargo?

- united-claims

- mortgage

- refinance

8 Answers 8

In lot of circumstances, the financial institution has recently generated their cash. Once you earn their financial is available so you’re able to traders even if the lending company remains upkeep they to have a charge. Therefore, for many who re-finance, they will sell it once again.

There will also be specific funny-currency explanations having to do with being able to amount so it while the a special sales.

It can be a good thing with the lender to refinance your loan for you – as you is staying the borrowed funds at that sort of facilities. This gives all of them longer to enjoy the fresh free currency you pay them from inside the appeal towards the kept longevity of the mortgage.

Banks that provide “Zero closing costs” is playing you to home loan payers usually move its mortgage to acquire the reduced interest levels – and you will anyone who retains the loan, has got the notice payments.

Banking companies benefit on stream origination fees. The newest “points” you have to pay otherwise closing costs is the primary benefit to the fresh financial institutions. An enormous most enough time threats of the mortgage are sold to a different group.

FYI, a similar is valid with resource banking institutions. In general, your order costs (which can be forgotten by the modern financing theory) are the fundamental material running new incentives to the community.

1- Wells Fargo cannot own our very own current mortgage. He’s bundled it and you may ended up selling it as an investment. 2- They generate their money away from ‘servicing’ the borrowed funds. Whether or not they merely score $50 four weeks so you’re able to service they (3% of our payment), that adds up to $fifty,000,000 per month if they have a million property below government. That’s $600 mil per year each million house becoming serviced step 3- Managing the escrow gets them more funds, as they can dedicate it and earn 2-3%. If the step 1,000,000 belongings possess an average equilibrium out-of $2,000 inside their escrow membership, they’re able to earn as much as $60 a year, otherwise $sixty,000,000 per year. 4- They make $step 1,000 if they re-finance our home. Here is the approximate cash right after paying genuine closing costs. Re-finance those billion homes, while generate a cool billion from inside the cash! 5- Nevertheless they desire to be sure that they continue united states while the a buyers. By minimizing the payment, it reduce steadily the likelyhood that people tend to refinance which have someone else, and we also are less likely to standard. (Not too they eradicate if we default, because they do not individual the loan!) 6- they make most gain settling the existing loan (they won’t contain it… remember), then packaging https://paydayloancolorado.net/walsenburg/ and you can promoting new home loan. Since they are attempting to sell it a security, they bring in coming worth, definition it sell all of our $200,000 loan for a great valuation regarding $360,000. Consequently they sell for $two hundred,000 Several tiny fraction of one’s most $160,000. Can you imagine they merely wanted a great ten% advanced of one’s $360,000 valuation. Meaning it offer all of our $200,000 loan having $236,000. It pocket $thirty six,000. Whenever they make a million ones purchases every year, that’s $thirty six mil dollars inside funds

$660,000,000 annually so you’re able to service the loan (Very little exposure, since it is are paid down by holder of mortgage while the a help percentage)

If they keep up with the funds for their life time (keep us away from refinancing that have other people…), they are able to build $19,800,000,000 (which is 19.8 million dollars inside the servicing charges)

Brand new earnings they generate in the a good refinance is a lot more than the money next helps make because of the carrying the borrowed funds having 29 years.