However, the consignment inventory accounting will be different for each party. The treatment will differ according to whether the consignor has transferred the goods to a temporary consignment inventory account. The person selling the goods is known as the consignee, whereas the one who provides the goods is the consignor. These two parties enter into a consignment agreement in which the consignee agrees to sell the items on behalf of the producer. The consignor pays the consignee for this service, but the consignor maintains ownership of the items while they remain unsold. Consignment is a good business model if you want to expand your retail business by being a consignee.

Damaged Items:

In consignment, the status of consignee is that of a commission agent. His income is the commission which he receives from consignor for the sale of goods dispatched to him. He has no share in the consignment profit because he is not a business owner or partner. Similarly, he is also not responsible for any loss incurred by the consignment business. However, the consignment accounting process can become difficult if you don’t know what you’re doing. By reviewing this guide and investing in good accounting software, you can make consignment accounting easy!

The 3 Basic Steps of the Consignment Process

- On 31st March 2018, Kent Ltd. sent his Account Sales showing that 80% of the goods had been sold for ₹60000.

- Your books have to be properly taken care of to ensure that everything will run smoothly.

- The consignee’s carelessness can cause serious losses to the consignor.

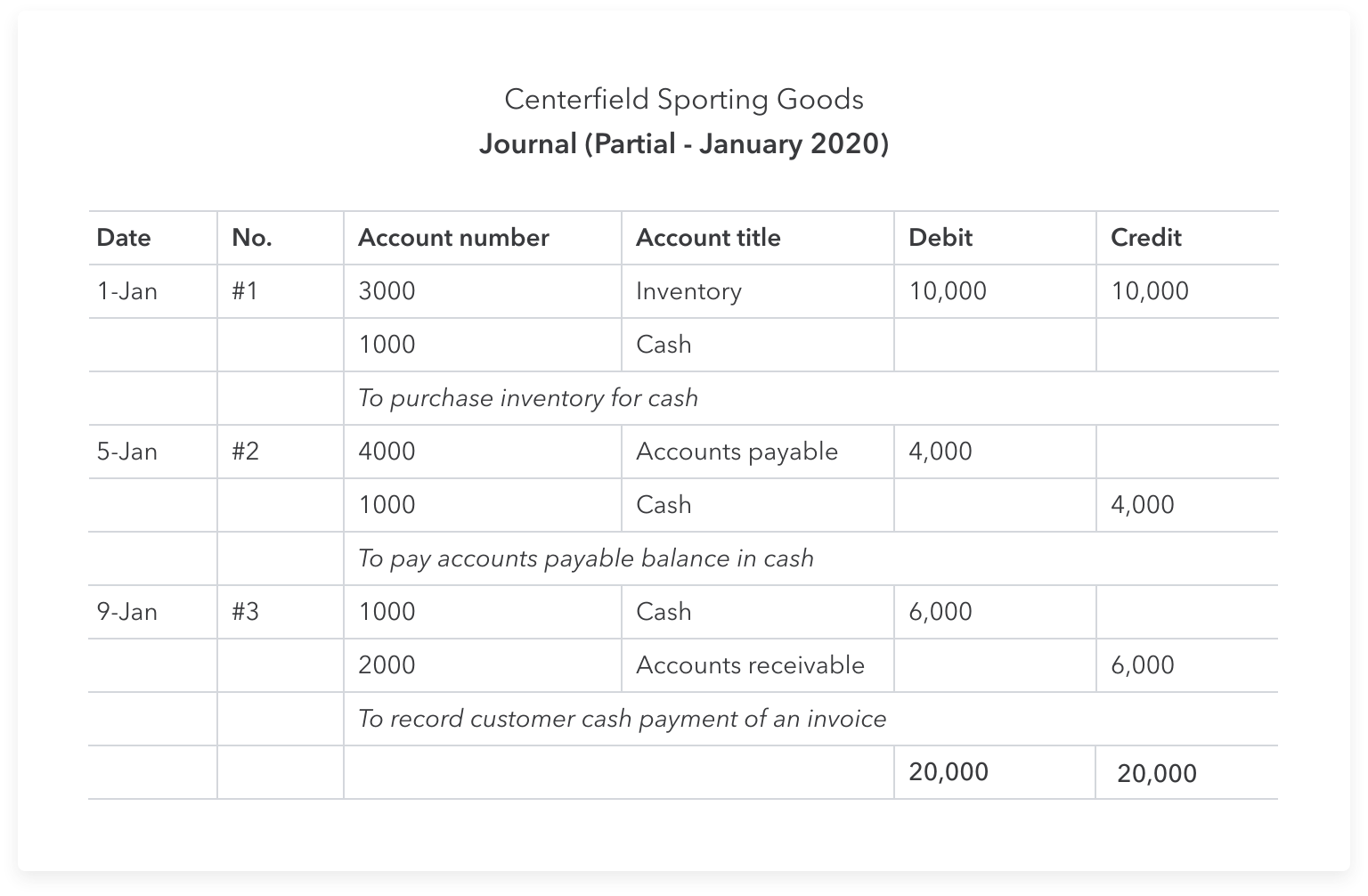

- The credit entry is to the personal account of the consignor and represents an amount due by the consignee to the consignor as the goods were sold on the their behalf.

In this example, we will assume for simplicity the goods are sold for cash. There are often hefty maintenance charges for goods that must be incurred by the consignee and increased shipping or transportation charges that the consignor must pay. For example, when the consignee’s and consignor’s locations are far apart. As an outcome of turbo tax 2011 for sale consignment, the consignor must pay a charge to the consignee, leading to a lower revenue ratio in the consignor’s control. Indirect costs include warehouse rental, warehousing charges, advertising expenses, wages, etc. The contrast between direct and indirect spending is critical, particularly when calculating the closing balance.

Consignment Accounting – Initial Transfer of Goods

It can help you track all of every part of the consignment accounting process. Consignment accounting is a financial practice that arises when a business agrees to sell products on behalf of another entity, known as the consignor. In this arrangement, the consignor retains ownership of the goods until they are sold to a third party by the consignee, who is the selling entity. The consignee essentially acts as an intermediary, promoting and selling the consignor’s products without taking ownership of the inventory. Once the consignee sells the inventory, the consignor can record the sale amount.

Before you consider entering a consignment inventory arrangement, you should discuss and agree on the conditions. On the flip side, the major benefits for suppliers are that your products get in front of more people, and customer loyalty is likely to improve with those customers you offer consignment options for. Inventory items that are sold through the consignment model are often perishable, seasonal, or previously owned. These developments underscore the potential legal and financial ramifications for the solar company as it grapples with the fallout from the alleged misreporting of crucial financial metrics. Consignment inventory is the way that consignor allows the consignee to sell the inventory without paying for it. The consignee will require to pay the consignor only when the goods are sold.

Parties in Consignment Account

For consignors, consignment is an opportunity to introduce your products to a different market. We hope this guide taught you how consignment inventory works and the different journal entries involved in the consignment process. As you can see, using double-entry accounting is the easiest way to record these transactions. When you’re looking to do this in the easiest way possible, make sure that you use reliable accounting software.

There has been no money transaction between Tony (the consignor) and Robert (the consignee), and Tony still owns the typewriter because there was no exchange. The consignee is entitled to three types of commissions on the sales of the goods. Shipping costs are inventoriable costs in the books of the consignor. These costs should be debited to the Inventory on Consignment account, not freight expense. The consignee also keeps a percentage of the sale proceeds and pays the consignor a predetermined sales amount.

Despite the various advantages mentioned above, there are a few factors from the other end of the spectrum that prove to be a disadvantage. The 2,450 reflects the profit made by the consignor on this consignment. The net effect of these postings is summarized in the memorandum income statement below.

Typical products sold through consignment include clothing, shoes, furniture, toys, music & other instruments, etc. Consignment accounting is a type of business arrangement in which one person sends goods to another person for sale on his behalf, and the person who sends goods is called the consignor. Another person who receives the goods is called the consignee, where the consignee sells the goods on behalf of the consignor on consideration of a certain percentage on sale.

The consignor is the owner of the goods and not the consignee though the possession is transferred. However, after the goods are sold the buyer becomes the owner of the goods. Here, we will discuss the accounting entries in the books of the consignee. Consignment indicates that one individual/business sends items to another individual/business to sell on account of the latter. The owner of the goods retains ownership; they maintain the right to the things.